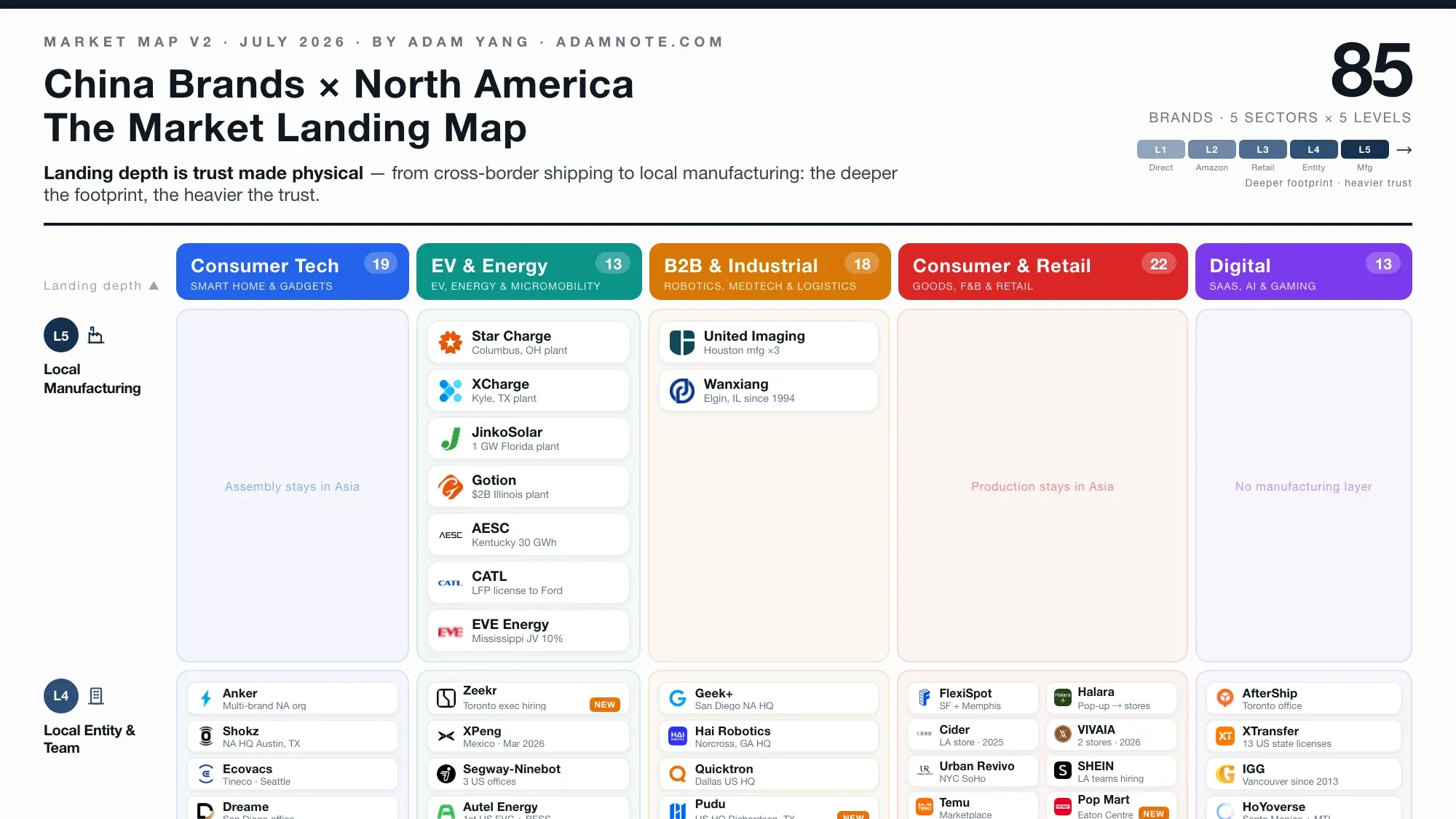

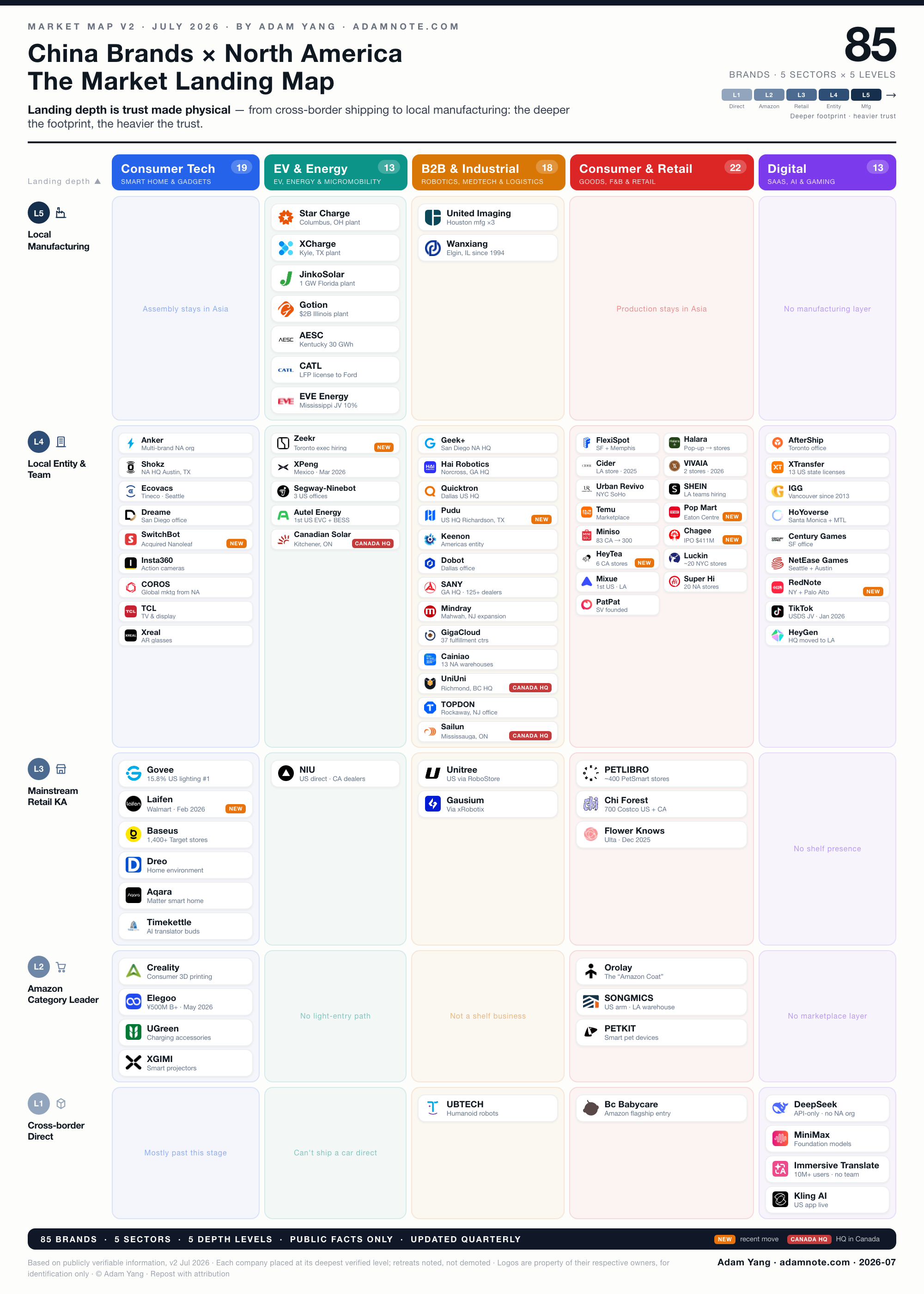

China Brands × North America: The Market Landing Map (v1, Mid-2026)

85 Chinese brands mapped by how deeply they have landed in North America: shelf, store, team, factory. Cheap trust is gone; landing depth is trust made physical. The most underpriced square on the map is Canada. Updated quarterly.

85 Chinese brands and companies, plotted on one chart by landing depth × sector. Every placement is backed by a specific, publicly verifiable fact — a retail channel, a store, a headquarters, a factory — not an impression. Data as of July 2026, updated quarterly.

For ten years, the standard question about Chinese brands abroad was “how are sales?” Revenue, rankings, growth rates. In North America in 2026, that question no longer tells you much. The better question is: how deep is the landing?

Whether a company ships parcels across the Pacific or pours concrete in Ohio is not a detail. It is the whole story. Because the thing Chinese brands used to buy cheaply, a customer’s first act of trust, has gotten expensive. Tariffs and the end of de minimis ate the price advantage. Amazon reviews stopped converting mainstream skeptics. What’s left is the slow way: put something physical where the customer can see it. A shelf at Costco. A store in SoHo. A local team. A factory.

That’s the thesis of this map: landing depth is trust made physical.

The framework

Columns: five sectors. Consumer tech & smart home · EV/energy · B2B/industrial · consumer goods, F&B & retail · digital/SaaS/gaming.

Rows: five levels of landing depth. Each company sits at the deepest level it has verifiably reached.

| Level | Meaning | Evidence looks like |

|---|---|---|

| L1 Cross-border Direct | Online cross-border, DTC, apps, or project exports; no local organization | Standalone site, app, API, dealer orders |

| L2 Amazon Category Leader | Top of an online category; maybe self-run warehouses; organization still in China | Amazon BSR leadership, own overseas fulfillment |

| L3 Mainstream Retail KA | On mainstream physical shelves or running a dealer network | Walmart / Costco / Target / Best Buy / Ulta / PetSmart / dealers |

| L4 Local Entity & Team | North American HQ, offices, own stores, distribution centers, local executives | NA HQ, direct retail, local hiring |

| L5 Local Manufacturing | North American factories, JVs, or technology licensing to local producers | Plants, JVs, licensing deals |

The map (85 companies)

| Depth | Consumer Tech & Smart Home | EV, Energy & Micromobility | B2B, Industrial & Logistics | Consumer Goods, F&B & Retail | Digital, SaaS & Gaming |

|---|---|---|---|---|---|

| L1 Cross-border Direct | — | — | UBTECH | Bc Babycare | DeepSeek · MiniMax · Immersive Translate · Kling AI |

| L2 Amazon Category Leader | Creality · Elegoo · UGREEN · XGIMI | — | — | Orolay · SONGMICS · PETKIT | — |

| L3 Mainstream Retail KA | Govee · Laifen · Baseus · Dreo · Aqara · Timekettle | NIU | Unitree · Gausium | PETLIBRO · Chi Forest · Flower Knows | — |

| L4 Local Entity & Team | Anker · Shokz · Ecovacs/Tineco · Dreame · SwitchBot · Insta360 · COROS · TCL · Xreal | Zeekr Intl (Geely) · XPeng · Segway-Ninebot · Autel Energy · Canadian Solar* | Geek+ · Hai Robotics · Quicktron · Pudu · Keenon · Dobot · SANY · Mindray · GigaCloud · Cainiao · UniUni* · TOPDON · Sailun | FlexiSpot · Halara · Cider · VIVAIA · Urban Revivo · SHEIN · Temu · Pop Mart · Miniso · Chagee · HeyTea · Luckin · Mixue · Super Hi (Haidilao) · PatPat | AfterShip · XTransfer · IGG · HoYoverse · Century Games · NetEase Games · RedNote · TikTok · HeyGen |

| L5 Local Manufacturing | — | Star Charge · XCharge · JinkoSolar · Gotion · AESC · CATL (licensing) · EVE Energy (JV) | United Imaging · Wanxiang | — | — |

* China–Canada hybrid entities (Canadian-registered, deeply tied to Chinese supply chains or capital), included as “bridge” cases.

Some obvious names (Bambu Lab, Roborock, DJI, Midea) are missing. Not because they don’t belong, but because I haven’t finished the evidence chain for v1. Inclusion discipline beats roster completeness; they’ll be in v1.1.

What the map shows: everything is moving deeper

Line up 85 companies by landing depth and something appears that no single news item shows: the whole chart is shifting toward depth. Not one company’s choice; a generation of companies moving at once. Three patterns stand out.

1. The Amazon champion’s rite of passage

Between 2024 and 2026, Chinese brands that own the top of an Amazon category walked into mainstream retail almost in single file. Laifen’s hair dryer hit Walmart shelves in February 2026 at $79.97. Baseus entered 1,400+ Target stores in October 2024. PETLIBRO put its AI litter box into nearly 400 PetSmart stores in March 2026. Flower Knows became one of the first Chinese color-cosmetics brands in Ulta in December 2025. Chi Forest (Genki Forest) reached 591 Costco warehouses in the US plus 109 in Canada.

The most telling case is Govee. North America is 83% of its revenue and it leads US smart ambient lighting at 15.8% share. Yet its IPO prospectus brags about cutting Amazon dependency from 76.6% to 65.6%. When the #1 player in a category treats leaving its home platform as an achievement, that tells you something: being an Amazon category champion is a ceiling, not a destination. Traffic costs keep rising and brand premium doesn’t follow. Meanwhile a Walmart or Costco shelf is the default trust list of the ordinary American household. Vendor onboarding, channel compliance, returns terms, local support — the annoyances are the moat. Whoever survives them first stops being a seller and starts being a brand.

2. DTC stopped pretending

The DTC story used to be that physical retail was the old world, waiting to be disrupted. Since 2025, the disruptors have been signing leases. Halara ran pop-ups in LA and Palo Alto and announced plans for flagship stores. Cider opened its first permanent store in LA (about 8,000 sq ft), with two more planned within the year. VIVAIA opened mall stores at Roosevelt Field and Garden State Plaza in spring 2026. Urban Revivo took 30,000 sq ft in SoHo, its largest store outside China.

The math forced the pivot: customer acquisition costs, tariffs, and the tightening of de minimis broke the pure-online model. A store you can touch became trust you can touch.

3. Factories go to America. Distribution goes to Canada. And the Canada gap.

The energy and industrial companies show a remarkably consistent division of labor. Manufacturing concentrates in the US: Star Charge in Columbus, Ohio (plus a Fremont Americas HQ and a 32+ GWh storage MSA signed in November 2025), XCharge in Kyle, Texas, JinkoSolar in Jacksonville, Florida (1 GW capacity after a $52M expansion), Gotion’s $2B plant in Manteno, Illinois, AESC’s 30 GWh plant in Bowling Green, Kentucky, United Imaging manufacturing all four imaging modalities in Houston and more than tripling its floor space in Pearland. The drivers are no mystery: tariffs, the IRA, and “made in America” procurement preferences. The friction is real too: AESC paused its South Carolina plant in June 2025 over tariff uncertainty, Gotion walked away from its Michigan project in October 2025, and CATL doesn’t build at all: its Kentucky arrangement is technology licensing, a workaround shaped entirely by politics. EVE Energy took the JV route in Mississippi with Cummins, Daimler Truck, and PACCAR, as a 10% technology partner; production is now pushed to 2028.

Canada plays a different role on this map, and for North American readers this is the part worth staring at. Canadian Solar runs its global headquarters from Kitchener, Ontario. Sailun runs its Americas arm out of Ontario with its own Canadian dealer network. SwitchBot acquired a controlling stake in Toronto’s Nanoleaf (per Matter Alpha) to get a North American retail distribution pipeline. GigaCloud’s and Cainiao’s fulfillment networks extend into Canada. UniUni, headquartered in Richmond, BC, runs last-mile delivery for SHEIN, Temu, and TikTok Shop across 80+ warehouses. HeyTea opened a Toronto distribution center in December 2025. Pop Mart announced a Toronto Eaton Centre store and at least ten more Canadian stores within the year. Miniso has 83 Canadian stores and targets 300 by 2030. Zeekr International spent April 2026 hiring an entire management team (sales, marketing, product) in Toronto to bring the Geely Auto brand into Canada.

Connect those dots, though, and the more striking thing is the blank space around them. For most Chinese companies, Canada is still something the US team covers on the side. The companies treating it as a market of its own — with its own organization and budget — can be counted on one hand. In a cycle where US policy risk keeps rising, that blank space is itself information. My read, and I’ll mark it as opinion: Canada is currently the most underpriced entry point on this map, and the handful of companies staffing it deliberately are early rather than wrong.

Why now

The three shifts share one underlying variable: cheap trust is gone. The first order bought with a low price is being eaten by tariffs and platform fees. Reviews accumulated online can’t carry brand recognition among mainstream buyers. So depth became the physical form of trust: a shelf is trust, a store is trust, a local team is trust, and a factory is the most expensive trust of all.

One honest caveat: this is the lens I use to read the map, not a law. Each company moved deeper for its own reasons — some ran the numbers, some were pushed by policy. The value of the lens is that it makes 85 isolated news events point the same direction. Whether the direction holds is what the next quarterly update is for.

How to read this map

Three rules:

- Position is a snapshot, not a ranking. L5 doesn’t beat L2. SONGMICS is thriving at L2; some L5 factories are paused. A position answers one question: how much has this company physically committed to North America right now?

- Each level up, organizational cost jumps an order of magnitude. L2→L3 takes channel compliance and retail BD. L3→L4 takes local hiring, local legal, local leadership. L4→L5 is capital expenditure plus political engineering. A large cluster of companies is stuck between L3 and L4: channel secured, organization lagging. That’s the highest-friction square on the map, and the most interesting one to watch.

- The blanks matter as much as the names. EV/energy has no L2 or L3: the sector offers no light-footprint option; you either stay out or go heavy. Digital products cluster at the extremes, L1 and L4: zero landing or full entity, almost nothing in between. Consumer goods and F&B have no L5 because the supply chain is still in Asia. Sector structure sets the shape of the path; companies only choose within it.

Data note: This map uses only publicly verifiable information — company announcements, listing documents, mainstream media reports, official channel pages. Company-sourced figures are labeled as such. Inclusion requires a verifiable North American landing action; absence from the map does not mean absence of business. v1 covers 85 companies and will be updated quarterly. Corrections welcome.

FAQ

What is "landing depth"?

A five-level framework for how much a Chinese brand has physically committed to North America: L1 cross-border direct, L2 Amazon category leader, L3 mainstream retail, L4 local entity and team, L5 local manufacturing. Each company sits at its deepest verified level.

Why is landing depth "trust made physical"?

Tariffs and platform fees ate the price advantage, and online reviews alone stopped converting mainstream buyers. A shelf, a store, a local team, or a factory is trust a customer can verify with their own eyes.

Which Chinese brands have entered mainstream US retail?

Between 2024 and 2026: Laifen into Walmart, Baseus into 1,400+ Target stores, PETLIBRO into nearly 400 PetSmart locations, Flower Knows into Ulta, and Chi Forest into 591 US Costco warehouses.

What is the "Canada gap"?

Manufacturing concentrates in the US, while distribution and headquarters functions grow in Canada: Canadian Solar in Kitchener, Sailun in Mississauga, UniUni in Richmond, BC. Yet most companies still run Canada as a side task of their US team, with no dedicated organization or budget.

How is this map sourced and updated?

Only publicly verifiable information: company announcements, listing documents, mainstream media, official channel pages. Every placement maps to one specific fact. Updated quarterly; v1 covers 85 companies.